CHFA’s Quarterly Housing Market Rundown: Q1 2022

Feb 08, 2022

At the Intersect, we know that predicting what the future holds isn’t as easy as looking into a crystal ball. Each quarter, CHFA’s Intersect housing blog will draw from staff and industry experts to provide market forecasts and analysis that will keep you up to date on the latest news and trends in Connecticut housing.

While a small state, Connecticut is comprised of many, diverse housing markets. Fairfield County is significantly influenced by what happens in New York City while eastern Connecticut’s housing market is impacted by its destination resorts and defense manufacturing. The state also has a variety of rental housing types, including single family attached and detached homes, a significant amount of small multifamily homes (2-4 units), and an abundance of adaptive reuse developments which were once office towers or old mills.

Vacancy Rates: Housing in Demand

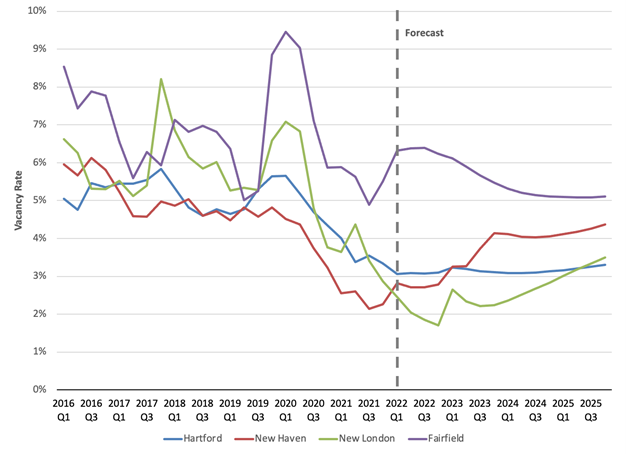

Demand for rental housing has remained strong in Connecticut through the pandemic with vacancy rates dropping in the state’s largest metro areas. Since Q1 2020, the Hartford metro, which includes Hartford, Middlesex, and Tolland counties, has seen vacancy rates drop from a near decade high of just under six percent to 3.3 percent (see Figure 1). New Haven County has experienced a similar drop in vacancy with a rate that currently hovers around three percent.

Figure 1 - Vacancy Rates in Connecticut’s Largest Rental Housing Markets

These low vacancy rates are likely impacted, in part, by inbound migration from both New York City and Boston. A strong home sales market that encourages some homeowners to sell their homes and rent for a period has compounded the issue. In particular, Fairfield County has benefitted from an influx of New Yorkers seeking homes with more space in nearby, relatively lower cost communities. The migration of New Yorkers into the county has had the dual effect of increasing homeownership and reducing multifamily rental vacancies.

Supply & Affordability

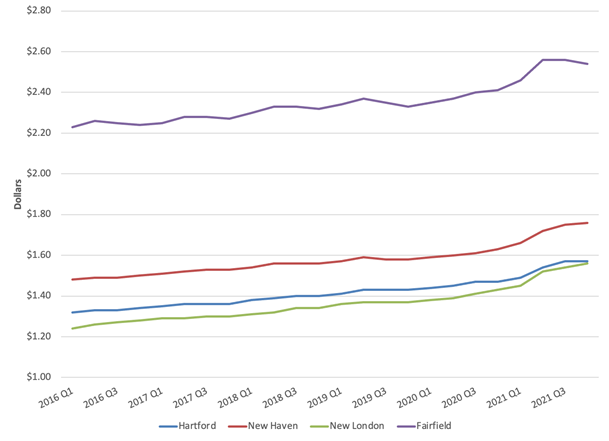

Increased demand and low vacancy rates tend to result in higher asking rents. Rent gains are occurring in all of Connecticut’s metros, contributing to increased housing costs for renters. For example, New London County is experiencing strong rent growth, posting an average annual gain of 4.9 percent over the past three years, the highest in the state (see Figure 2).

Figure 2 - Asking Rent per Square Foot by Rental Market

As rents increase and demand tightens, new construction projects are feeling the pinch of labor shortages, higher labor costs, and supply chain issues. As such, the number of new affordable units coming online in the state has been slowed. In 2019, just over 1,000 new units of CHFA-financed was completed compared to just 636 in 2020 and 502 in 2021. Rehabbed units have experienced a similar decline from 1,359 units in 2019 to just 592 in 2021. Such a trend is unsurprising given the effects of COVID-19 on the construction industry. Units that otherwise would have been completed in 2020 or 2021 have been delayed as projects work through supply chain delays and seek creative solutions to growing project budgets as the price of goods has skyrocketed. A recent national survey of non-residential contractors indicates that the availability of skilled workers and supply chain issues continue to be top concerns for the construction industry coming into the New Year, followed closely by economic uncertainty and material costs. Delays will likely continue in 2022 as developers try to procure supplies and find additional dollars to cover any budget gaps due to increased costs.

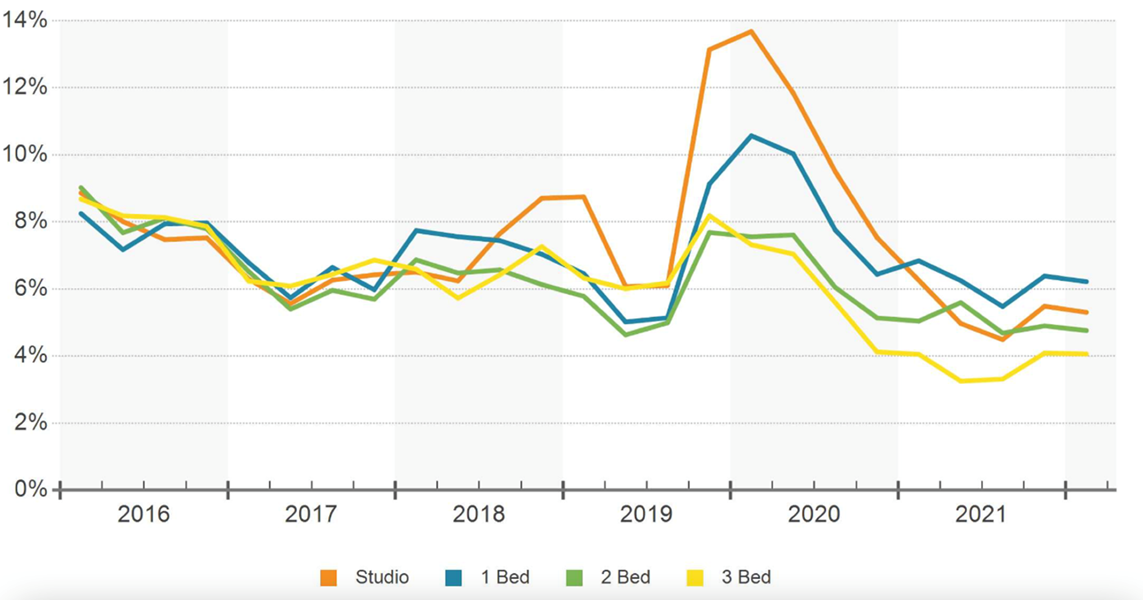

The pandemic has forced many companies to let their employees work from home. As employers consider the permanency of this trend toward remote work, a potential new reality has led to renters wanting more space. This is particularly true in Fairfield County where the vacancy rate for three-bedroom apartments declined at the onset of the pandemic and is currently lower than apartments with fewer bedrooms (see Figure 3).

Figure 3 - Vacancy by Bedroom Size - Fairfield County Rental Market

This drive towards larger rental homes has been slow to be reflected in the affordable market. A review of applications submitted for the 2021 9% Low Income Housing Tax Credit program, a significant source of new affordable units in the state, showed preference towards studios and one-to-two-bedroom units, which made up 87% of proposed development. This number was up three percentage points from the preceding year in which 84% of units contained less than three bedrooms. Despite the overall market desire for larger units, the inclination towards smaller units in the affordable market is unsurprising. Given the lengthy process from pre-development to application, developers in the 2020 and 2021 rounds had limited ability to respond to the need for larger units as a result of the pandemic. The 2022 LIHTC 9% applications, which were submitted to CHFA in January, have provided a first glimpse of the development community’s response to this market shift. In fact, the percentage of units with less than three bedrooms is down, making up just 76% of total proposed development. Overall affordable development size seems to be on the decline. In 2020, the average LIHTC application size was comprised of 65 units compared to 58 units in 2022, a decrease of 11%. This may be a reflection of the aforementioned labor shortages and increased construction costs, which could drive developers to focus on smaller projects to fit into tighter budgets.

Trends to Watch

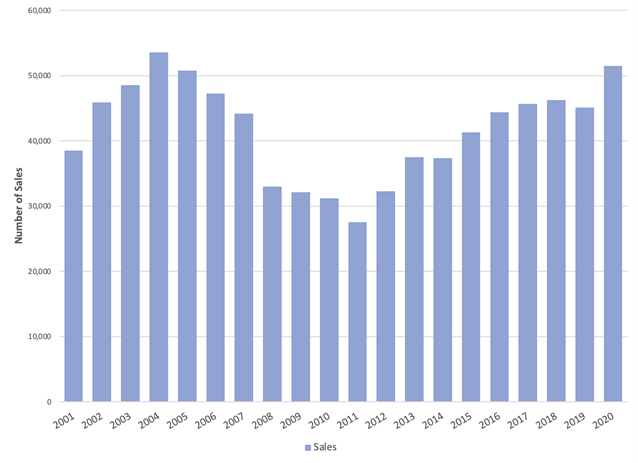

While a growing trend since 2011, during the pandemic investors have purchased Connecticut single-family homes, possibly with the expectation of meeting the market demand for larger rental options. This trend impacts both the rental market as well as the homeownership market, as production of affordable single-family homes has dramatically declined throughout the state. With supply low and demand still high, the market will likely continue to be in favor of the seller when the homebuying season kicks off in March. As such, buyers, particularly low-to-moderate income ones, will face challenges in finding properties within their limited budgets. For further reading on this, check out the Intersect’s series on Starter Homes in the state.

Figure 4 - Single-Family & Condominium Investor Buyers in Connecticut

Looking ahead, it’s clear that the impact of COVID-19 on both the single and multifamily housing markets will continue into 2022. As renters and homeowners alike spend more time in their homes, it’s as important as ever to provide a diverse housing stock in price, location, and size to accommodate the needs of all residents.

Stay tuned for the Quarter Two market forecast where the Intersect will provide updates on all things housing. Have questions or insights you’d like to share? Send a message to research@chfa.org to get in touch with our team.

Want to get the next report sent right to your inbox? Visit www.chfa.org/signup and select the "The Intersect - CHFA's Housing Research Blog."

****

Jonathan Cabral is a Manager in the Research, Marketing, and Outreach department where he investigates the intersection of housing policy, planning and economics. He is a certified planner and holds a BA in International Studies and an MA in Public Policy from Trinity College. He is currently a PhD student of Geography, studying urban planning and policy at Birkbeck, University of London.

Kayla Giordano is a Senior Program & Data Analyst in the Research Marketing and Outreach department. She holds degrees in Political Science and Economics from Eastern Connecticut State University as well as a MA in Community Development Policy & Practice from the University of New Hampshire.